How do you analyze a “high growth” company to determine whether to invest your hard earned dollars? This is the 3rd in a series of posts on the topic. The first two can be found here:

20 Fundamental Investing Criteria : Segment 1 of 10

Fundamental Investing Criteria : Segment 2 of 10

In my first post, I summarized all 20 fundamental metrics I utilize to analyze the strength, performance and excellence of a high growth company that I may choose to invest in…one of only 10 companies that will make the portfolio cut.

Today I will focus on number 5 of 20 criteria that I analyze:

#5) Future Growth Indicators: Customer, product, geographic & other growth indicators (All 20 criteria are summarized at the bottom of this post).

How can we predict growth? How can we see it BEFORE it happens?

Growth of a company comes in many forms. I covered the first and probably the most important criteria for any fast growing company, “Rapid Revenue Growth” in the very first post (see link to post above); however, revenue growth is “backward” looking at the past 3 or 12 months revenue and compared to the year prior period.

How do we get an indication a company is accelerating its growth before they announce it in their earnings release? Is their a way to glean an advantage? I believe there are several!

There are several forward looking indicators one can assess to get an indication of future revenue growth, because make no mistake, “revenue” growth is probably the most important and critical growth factor to monitor and to ensure in order to be a successful “high growth” company. Without revenue growth, it is difficult to impossible to continue to invest in the necessary R&D, S&M or G&A expenditures…and forget about attaining or increasing profitability, the end financial goal of every company. So how can we predict revenue growth?

Very simply. We can look at a company’s growth in any number of other organic and inorganic areas that the company actually tracks and provides us in various company presentations, earnings calls, and quarterly earnings releases, including the following:

- Number of total new customers and their growing customer base

- Growth of existing and larger (in particular) customers

- New products or offerings by the company

- Geographic growth outside of existing geography or customers

- Growth into new market segments

- Inorganic growth such as acquisitions of companies and/or competitors

- Growth of billings, backlog, deferred revenue and/or RPOs

- Employee headcount growth…especially in Sales & Marketing

- Growth in revenue from existing customers (measured using NDBRR)

There are no doubt many other growth factors one can track depending on the company, industry, etc. The most important takeaway here is to figure out what those growth factors and metrics are for each company and analyze these leading indicators to get an idea of what direction a company’s revenue growth is possible or likely to go. It will give you critical advance notice of when a company’s growth is accelerating or decelerating…and in what direction. This in turn will help you make an education decision if and when to invest, continue to hold, add to a position or, potentially, sell it.

Example: Docusign (DOCU) is a great example of a company that is exhibiting growth in almost all of the areas listed above.

- >1 million total customers and 42% CAGR in customers since 2018.

- 136,000 enterprise(large) customers and 54% CAGR in customers since 2018.

- Three new product lines introduced beyond their primary “e-Signature” product include Contract Lifecycle Management (CLM), Insight, and Notary.

- DOCU had 84% q/q international growth last quarter, which now makes up 21% of revenues (i.e. plenty more room to grow). They are currently expanding into 8 new international country markets (many in Europe) directly and already have a presence in 180 countries!

- With their new product offerings (listed above), DOCU is expanding into legal contract management and analysis, as well as notary services. They are also becoming far more widely accepted across all industries (like mortgage and real estate transactions) since Covid-19 forced their widespread use.

- DOCU continues to grow both organically, as shown in these examples here , but also in-organically through precision acquisitions when necessary of technology including LiveOak Technologies most recently in July 2020.

- Billings grew annually more than 54% last year…an indication of future revenue to be recognized.

- Annual employee headcount last fiscal year increased from 4,281 up to 6,080…up 42%!

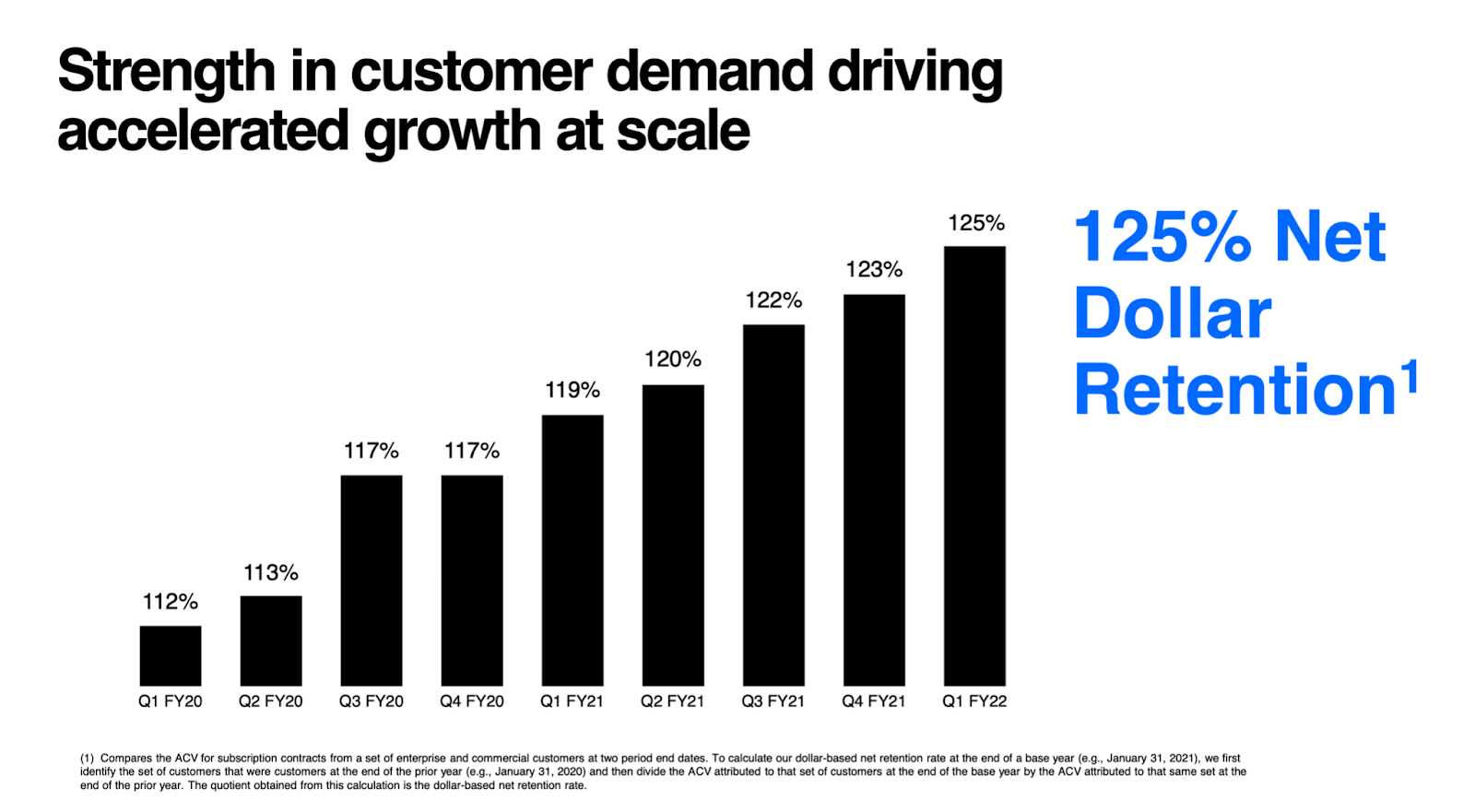

- Net Dollar Based Retention Rate (NDBRR) is roughly the increased (or decreased) average spending by existing customers in a year. I will cover it in my next post, but roughly, any number over 100% means you are losing NO average existing customer spend from beginning to end of year…in DOCU case, they are actually increasing their existing customers spend by 125% and even that number has increased in the past 6 quarters!!

It is absolutely no surprise then, when I consider all the above growth factors together that both Subscription revenue and Total revenue growth have continued to ACCELERATE nicely every single quarter for the past 6 quarters (note that subscription revenue made up over 96.3% of total revenue last quarter):

This is a large company with an annual revenue run rate of $1.8B dollars that is already growing (and accelerating) at 61% q/q; but absolutely NOT sitting on their haunches as they expand their product lineup, their international presence, their billings, their large (and small) customers….and, of course, their headcount to support all their growth and future growth! This is the kind of company and growth I look for and that I get VERY excited to invest in!!

I hope this has been instructive and helpful. Next post I will cover #6 below…what I refer to as: Management FLESH: (F)ounder (L)ed, (E)xperienced, (S)H friendly, (H)onest.

Cheers! – Poleeko

=============================================================

20 Fundamental Criteria for Investing in high-growth companies:

- Rapid Revenue Growth (Q/Q & Y/Y); greater than 35% & accelerating

- ARR – Annual Recurring Revenue Model (usually subscription based)

- Company Size: Market Cap and Trajectory – Ability to 5-10x itself

- TAM (Total Addressable Market) & Runway – Ability to 5-10x itself?

- Growth Indicators: Customer, product, geographic & other growth

- Management FLESH: (F)ounder (L)ed, (E)xperienced, (S)H friendly, (H)onest

- Net Dollar Based Retention Rate min > 100%; prefer >120%

- High Gross Margins min > 50% – stable or increasing – Prefer 70%+

- Balance Sheet – Strong “going concern” (Strong Cash with little or no debt)

- EV/Sales – Understand this number is NOT created equal across companies

- Competitive Advantage: New technology…Leader…Moat…or a niche

- Improving Operating Leverage (Decreasing expenses to revenue ratio)

- Insider & Institutional Ownership (and founder led is a huge plus)

- Consensus: Motley Fool, Seeking Alpha, Bert, IBD, Institutional buying

- US based Company – No Chinese companies

- Minimal or limited Cap-Ex requirements – Ability to pivot quickly.

- Positive or rapidly improving CFFO and FCF

- Profitability or the ability to get there quickly

- Little or no competition unless they are the clear sector leader

- Increasing (hopefully rapidly) earnings (if not rapid revenue growth)

I will reiterate that this is by no means an exhaustive list, but covers many of the more critical KPI’s that I follow when investing in high growth, cutting edge companies.

Phenomenal Victor! Thank you for another great lesson in investing!